🌱 The Power of Compounding

It’s not wrong when someone says “Compounding is the eighth wonder of the world.”

When I was studying finance with excel, an interesting activity was to just see how much money I can pass on to my future child with my current networth assuming continuous compounding.

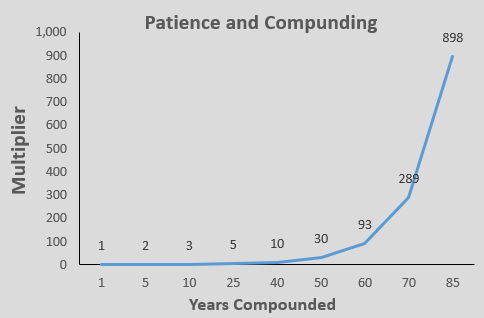

To, understand what that means, Look at this simple graph:

If you invest money that compounds at 12% annually, by the end of 40 years, your original amount becomes 10 times larger. But here’s where it gets fascinating — wait just 10 more years, and that same investment doesn’t just double; it grows to 30 times your original amount.

That’s the magic of compounding — growth feeding on itself, returns amplifying future returns.

💡 What Is Compounding, Really?

At its core, compounding is money working to create more money. Every period, your returns generate more returns. It’s financial snowballing — small gains rolling forward, turning into huge outcomes given enough time.

But compounding isn’t always your friend. It’s neutral — it simply amplifies whatever side you’re on. You make or lose money playing with compounding.

That’s why understanding compounding is foundational for nearly every financial decision you’ll make.

🏦 Compounding in Everyday Decisions

1. Choosing Between Loan Offers

Say two banks offer you loans at 10% interest:

- One uses simple interest.

- The other uses compounding interest.

Which one costs more?

The compounded loan, of course. Because the interest itself make you owe more interest. If you’re borrowing, compounding works against you — your liability grows faster than you expect. This especially becomes a trap, if you miss a EMI.

This is why small rate differences (like 11.5 % vs 12%) matter more than most people think. Over time, compounding magnifies every decimal. The earlier graph showed 12% compounding gave you 30 times return in 40 years whereas a 11.5% return will give you 26 time the return. The price for 0.5% is 4 times your investment.

2. Dividend Reinvestment vs Spending

Now imagine you own a stock giving a 15% total return, including dividends.

If you reinvest those dividends, your money compounds at the full 15%. If you spend them, your effective compounding rate drops — maybe to 12% or less — because some of your capital stops working for you.

The choice between reinvesting or using your dividends is essentially a choice between future compounding and present consumption.

if you choose to reinvest dividends, they keep growing at a faster pace.

⚖️ Rule of Thumb

🧭 Compounding is good when it works for you — bad when it works against you.

| Compounding Works For You | Compounding Works Against You |

|---|---|

| ✅ Reinvesting dividends | ❌ Owing high-interest loans |

| ✅ Holding quality assets long-term | ❌ Frequent trading and transaction costs |

| ✅ Staying patient with investments | ❌ Letting credit card debt roll over |

In other words: 👉 Be on the earning side of compounding, not the paying side.

🧮 Compounding Levers

The effect of compounding can be controlled by various factors. they are time, initial principal, rate of return and incremental addition.

Theoretically the formula is simple – Principal x (1 + interest per period)(No. of Periods). You can increase the final amount by managing any variable. If you cant find a higher initial amount to invest, you can compensate by having longer period. If the rate of return is high enough, you could have lower no. of period. You can also keep adding more money into the scheme resulting in a larger money pool by end of the term.

🏦 Impact of Taxes and Transaction Cost

One of the easiest ways to destroy the benefits of compounding is by creating frequent taxable events. Every time you buy and sell an investment in pursuit of slightly higher returns, you trigger taxes and transaction costs — both of which erode your long-term growth.

A taxable event occurs when you sell an asset and the government takes its share of the gain. The goal should be to allow your money to compound silently, without unnecessary interruptions. Each time you sell and pay taxes, a piece of your compounding engine is handed over to the tax system.

In many cases, it’s even smarter to take a temporary loan rather than break a high-compounding investment. Paying 10% interest on a loan might be cheaper than paying 25–30% in taxes on realized gains.

Understanding the tax impact on compounding is critical — it helps you decide when to let compounding continue and when it’s worth interrupting. In finance, patience isn’t just a virtue — it’s a strategy that protects your compounding from the silent drag of taxes

💬 Closing Thought

Compounding is not a trick; it’s a law of financial gravity.

Is getting $1 million every day for 30 days better, or starting with $1 on day one and doubling it each day? It’s an age-old question — but it perfectly shows the hidden, explosive power of compounding

It can build wealth quietly or erode it silently — depending on which side of it you stand.

Albert Einstein reportedly said: “He who understands it, earns it; he who doesn’t, pays it.” So, before every financial decision, ask: “Am I letting compounding work for me — or against me?” Because the eighth wonder of the world is not a myth. It’s math — multiplied by time, and its omnipresent.

A 1% rise each month sounds harmless — until you realize it doubles in five years. Compounding hides its power behind small numbers, then reveals it all at once.